But what can we do about it?

Let's consider a few scenarios for buying a house:

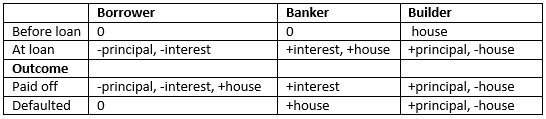

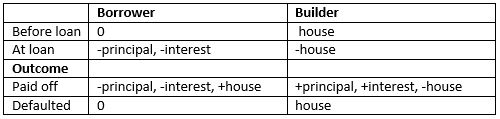

1. In the current system the borrower approaches the bank, negotiates the terms, pays off the loan and interest, and hopefully owns the house at the end.

We are all familiar with this, but please note the following:

- The currency did not come into existence until the borrower was approved, and signed a promissory note with the terms of the agreement. Then the bank created the currency (out of nothing, a bookkeeping entry) for the builder to be paid. This promissory note becomes an asset at the bank, that can be traded (sold) if desired.

- At the start the bank had nothing, but at the end the bank had either the interest payments (often many times the principal), or the house. In other words the bank benefited without any assets to start with.

- Also important to note is that the bank created only the principle. The interest was drawn out of the mainstream economy, reducing the currency supply, and creating the need for more and more borrowing just to pay interest and maintain liquidity.

2. In this first scenario above, the currency can be inflated almost without throttle. Some countries, such as Canada and the UK, have no reserve requirements, but even those with fractional reserve requirements can multiply the currency, and even borrow the small reserve from the central bank.

In the second scenario, mandating a 100% reserve requirement means banks cannot create currency, but are custodians of savings which they can lend to borrowers, much like Savings and Loans, or Credit Unions.

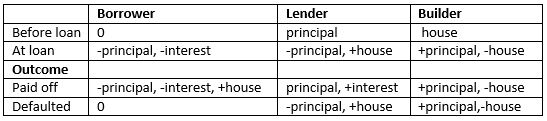

The builder might be in a position to do the financing without an intermediary.

Unless the interest earned is returned to the mainstream economy, we still have to deal with the deflation of the currency supply as interest is paid out of principals.

3. Thirdly, let us consider an ideal world

- Without interest on the currency supply,

- Price stability (currency inflation matching economic activity), and

- Full employment

Recall that the banker does not create the currency to pay the builder until a promissory note is signed by the borrower. It is on the strength of the promissory note that the currency is created out of nothing.

If currency is created out of nothing, and the promissory note is the authorisation for the amount, why not simply pass the promissory note through to the builder without the bank, ie. the promissory note is the currency. Just as the bank could trade promissory notes, so the builder can use it to make payments.

What about gold or crypto currencies?

Gold has been successful at providing trust and as a hedge against inflation. Cryptos such as Bitcoin behave similarly.

The snag is that we either need fiat to acquire gold / cryptos (like commodities), or we need to mine them (and managing our currency supply through the rate of mining is not accurate enough for price stability).

Mechanics

Rating an issuer of a promissory note (ie. self-issued currency) would be the same tried and tested way that banks evaluate potential borrowers on debt, income, assets, reliability, etc.

If the issuer is found to be good for the amount, the promissory note is accepted as currency and the transaction takes place. Trust and confidence in this note is the result of the vetting algorithm.

Examples of other forms of trust are whether the document can be exchanged for gold, or having expensive crypto mining rigs ensure the incorruptibility of the transactions.

Considering that banks are trusted with our currency (completely under their control; even controlling our access to our own currency) on the flimsy promise to pay the bearer (account holder) the amount in currency, which simply means a piece of paper with an amount printed on it - no gold, no crypto, no promise of performance.

A beneficial new world

- Our money in our own crypto wallets, under our control, and

- A currency based on trusted notes for real economic activity.

Not inflated paper created out of nothing, issued as debt, charged at interest, under complete control of banks, crushing society into dispossession and destitution.

Self-funding (bank-free currency)

Nice information on here, I would like to share with you all my experience trying to get a loan to expand my Clothing Business here in Malaysia. It was really hard on my business going down due to my little short time illness then when I got heal I needed a fund to set it up again for me to begin so I came across Mr Benjamin a loan consultant officer at Le_Meridian Funding Service He asked me of my business project and I told him i already owned One and i just needed loan of 200,000.00 USD he gave me form to fill and I did also he asked me of my Valid ID in few days They did the transfer and my loan was granted. I really want to appreciate there effort also try to get this to anyone looking for business loan or other financial issues to Contact Le_Meridian Funding Service On Email: lfdsloans@lemeridianfds.com / lfdsloans@outlook.com He also available on WhatsApp Contact:+1-9893943740.

ReplyDelete